Portfolio Management And Investment Horizon

We can’t discuss about portfolio management without mentioning Investment Goals and Investment Horizon. For the former please refer to this page.

Investment horizon is a term used to identify the length of time an investor aims to maintain their portfolio before selling their securities for a profit.

Investment horizons can range from very short-term, just a few days long, to much longer-term, potentially spanning decades. For example, a young professional would have an investment horizon spanning decades. However, a corporation’s treasury department might have an investment horizon that’s only a few days long.

When investors construct an investment portfolio, establishing an investment horizon is one of the first steps they must take.

The length of an investment horizon will often determine how much risk an investor is exposed to and what their income needs are.

Generally, the shorter the investment time, the lower the risk and returns. The longer the time of investment the higher the risk and return.

Individuals in their early investing years are the most likely to have longer-term investment horizons. Seasoned or older investors are more likely to use a shorter horizon because they have less time to realize profits.

Individuals with a longer investment horizon can take on more risk since the market has many years to recover in the event of a pullback; this is because there is more time to make a profit from investments or recover from losses sustained, hence making riskier investments with the potential for a greater payoff down the road is appropriate.

For example, an investor with an investment horizon of 30 years would typically have most of their assets allocated to equities.

Beyond that, an investor with a long-time horizon may invest their assets in what are considered riskier types of equities, such as mid-cap and small-cap stocks. These types of stocks, or sub-asset classes, tend to exhibit much larger price swings over short periods than large-cap stocks because they tend to be less well-established and more susceptible to outside economic forces.

Thus, while they may be risky for investors with shorter investment horizons, these short-term swings have little to no impact on investors looking to hold on to those stocks for many years.

Investors should adjust their portfolios as their investment horizon shortens, typically in the direction of reducing the portfolio’s level of risk. For example, most retirement portfolios decrease their exposure to equities and increase their holdings of fixed-income assets as they near retirement.

Fixed-income investments typically provide a lower potential return over the long run relative to stocks, but they add stability to a portfolio’s value since they usually experience less pronounced short-term price swings.

Portfolio Management: Categories of Investment Horizons

SHORT-TERM INVESTMENT HORIZON

A short investment horizon usually doesn’t exceed a period of three years.

This investment time frame, as mentioned above, is typically best for individuals in their later years, preparing for retirement. However, it may also be appropriate for individuals who are strongly averse to risk or need to access a significant amount of cash in the near future.

For risk-averse investors, it’s best to have guaranteed assets or securities, including savings accounts, certificates of deposit, and bank deposits.

MEDIUM-TERM INVESTMENT HORIZON

Investors who are less risk-averse and not looking for cash for retirement or a large purchase are better suited to a medium-term investment horizon; this usually means a period of three to five years. Investors with this type of investment horizon are between low and high risk, meaning a conservative and diversified portfolio is best, mixing investments in both stocks and bonds. The ratio of stocks to bonds should be determined by the individual’s specific wants and needs.

LONG-TERM INVESTMENT HORIZON

Finally, a long-term investment horizon of 5 years and above is appropriate for savers willing to take large risks for large potential rewards. In most cases, the long-term investor’s portfolio includes a significant amount of higher-risk investments with potentially higher returns. The majority of the portfolio should therefore consist of shares and, to a lesser extent, bonds.

Intelligent Investing View About Portfolio Management

We believe the goal of every investor should be to make the most out of the capital invested while reducing the risk as much as possible.

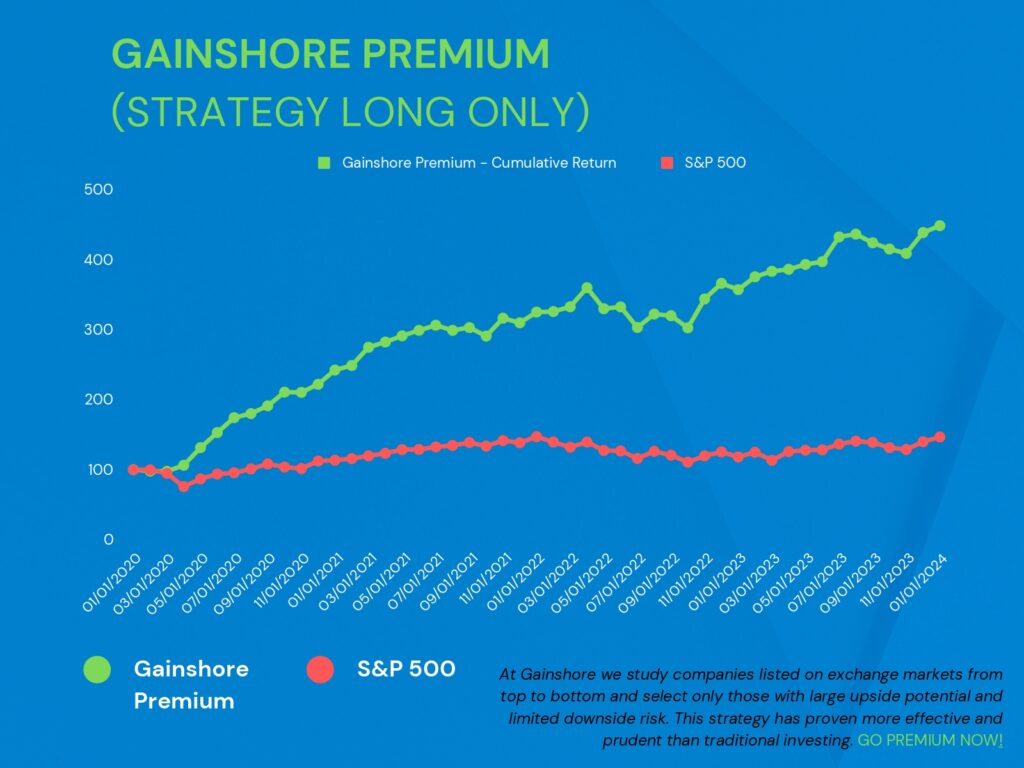

At the point of writing, there is nothing better than Intelligent Investing to fulfil this requirement, which is why Gainshore was ultimately born.

Secondly, it should not be your age what drives your portfolio allocation but your personal situation. For example, you can be 85 years old, but if your retirement pension is more than enough for your spending and you have plenty of savings, for no reason on earth you should be buying bonds and avoiding stocks – you should actually do the opposite. Vice versa, maybe you are 25, have three kids, and all your and your partners’ savings will be needed in a few years’ time for an already planned house purchase or down payment, then you should avoid investing altogether.

Today, more than ever, the best genuine way to make sound profits is to invest in equity stocks with considerable upside and limited downside risk. With the central banks’ monetary policies involving large money printing and purchasing securities to avoid global recession risk (read also 4 Reasons Why Should you Invest to Protect Yourself from Inflation), bonds have lost their defensive nature and the traditional function of being negatively correlated to stocks; moreover, the rate of return that bonds offer is, in our view, inappropriate (and sometimes negative!) The only fixed-income securities offering modest returns are called high-yield, or junk, for one reason: they are risky! And require expertise.

Unless you are an institutional investor with investment allocation rules to abide by, we believe it is not worthwhile to deploy money into fixed income or other similar asset types; the return you are going to make is not high enough to compensate for the risk you are bearing.

However, wary that things may change in the short run, we would promptly revise our stance if that is the case.

Before investing, read carefully the 15 Investing Mistakes to Avoid, check if you have them all and, if you feel comfortable, start prioritising most of your funds in intelligent stocks, equity funds, and ETFs.

Our advice is to invest only the capital you are ready to risk losing and leave the rest in cash.